Effective liquidity management is the lifeblood of any successful business. It’s not just about having enough cash on hand; it’s about strategically managing cash flow, anticipating needs, and mitigating risks to ensure consistent operations and sustainable growth. This guide explores the multifaceted nature of liquidity management, from forecasting cash flow and optimizing working capital to navigating short-term financing options and developing long-term strategies.

We’ll delve into practical strategies, real-world examples, and the crucial role of technology in maintaining a healthy financial position.

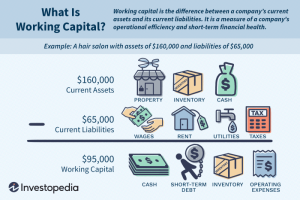

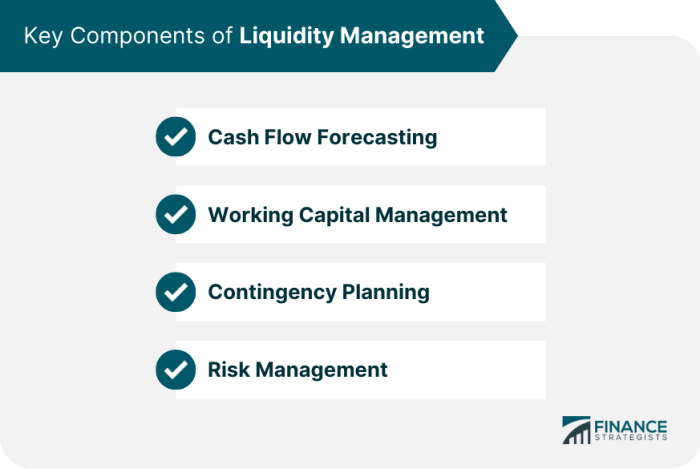

Understanding liquidity management involves a deep dive into various aspects of financial health. This includes mastering cash flow forecasting, which helps predict future financial needs and enables proactive planning. Efficient working capital management, encompassing inventory control and accounts receivable/payable, is equally vital. Choosing appropriate short-term financing options and developing robust long-term liquidity plans are also critical components for ensuring business resilience and success.

We’ll also explore how integrating technology and understanding the interconnectedness of logistics and liquidity can optimize your financial performance.

Short-Term Financing Options

Effective short-term financing is crucial for businesses to manage cash flow, fund immediate operational needs, and seize time-sensitive opportunities. Choosing the right option depends heavily on the company’s specific financial situation, industry, and risk tolerance. Several key options exist, each with its own set of advantages and disadvantages.

Lines of Credit

A line of credit is a pre-approved loan amount that a business can borrow against as needed. It functions like a revolving credit card, allowing businesses to draw funds up to the approved limit, repay them, and redraw as necessary. This flexibility makes it a popular choice for managing unpredictable cash flow fluctuations.Advantages of lines of credit include readily available funds, flexible repayment terms, and the ability to only pay interest on the amount borrowed.

Disadvantages can include potentially high interest rates, fees associated with the application and maintenance, and the possibility of impacting credit scores if not managed responsibly. For example, a small bakery might use a line of credit to cover unexpected ingredient cost increases or seasonal demand spikes.

Invoice Financing

Invoice financing, also known as accounts receivable financing, provides immediate cash flow by advancing a percentage of the value of outstanding invoices. Businesses essentially sell their unpaid invoices to a financing company, receiving a quicker payment than they would waiting for their customers to pay.This option offers quick access to capital, particularly beneficial for businesses with long payment terms from clients.

However, disadvantages include potentially lower advances (receiving less than the full invoice value), ongoing fees, and the relinquishing of control over the collection process to the financing company. A construction company, for instance, might utilize invoice financing to accelerate payments from large clients with extended payment schedules, thus improving their short-term liquidity.

Factors to Consider When Selecting Short-Term Financing

Choosing the appropriate short-term financing solution requires careful consideration of several factors. It’s not a one-size-fits-all scenario.

- Amount of funding needed: How much capital is required to address the immediate need?

- Length of time needed: How long will the business require access to the funds?

- Interest rates and fees: What are the total costs associated with each option?

- Repayment terms: What are the repayment schedules and penalties for late payments?

- Creditworthiness: What is the business’s credit score and its impact on eligibility for different financing options?

- Collateral requirements: Does the financing option require collateral (assets pledged as security)?

- Impact on business operations: How will the chosen financing option affect daily operations and future financial planning?

Long-Term Liquidity Planning

Securing a business’s long-term financial health requires a proactive approach to liquidity management. Unlike short-term strategies focused on immediate cash flow needs, long-term liquidity planning anticipates future demands and ensures the business has sufficient resources to navigate potential challenges and capitalize on opportunities. This proactive approach minimizes financial distress and enhances the overall resilience of the organization.Long-term liquidity planning involves forecasting future cash flows, identifying potential liquidity gaps, and developing strategies to mitigate risks.

It’s a crucial element of strategic financial planning, interwoven with the business’s overall growth strategy and risk management framework. A well-defined plan provides a roadmap for sustainable growth, enabling informed decision-making related to investment, expansion, and operational efficiency.

Methods for Developing a Long-Term Liquidity Plan

Developing a robust long-term liquidity plan involves a systematic process. This includes comprehensive financial forecasting, scenario planning, and the implementation of appropriate financing strategies. The process should be iterative, regularly reviewed, and adapted to changing market conditions and business performance.A crucial first step is to create detailed financial projections. These projections should extend several years into the future and incorporate various assumptions about revenue growth, operating expenses, and capital expenditures.

Sensitivity analysis should be conducted to assess the impact of various scenarios on projected cash flows. This allows businesses to identify potential liquidity shortfalls and develop contingency plans. The next step involves identifying potential sources of long-term funding, including debt financing, equity financing, and internal financing strategies. This evaluation should consider the cost of capital, the flexibility of each financing option, and the impact on the business’s financial structure.

Scenarios Impacting Long-Term Liquidity

Several scenarios can significantly impact a business’s long-term liquidity. Understanding these potential challenges is vital for developing a resilient liquidity plan. These scenarios can range from predictable events, such as seasonal fluctuations in demand, to unexpected disruptions, such as economic downturns or natural disasters.For example, a significant increase in raw material costs could severely strain a company’s cash flow, especially if it lacks sufficient working capital reserves or readily available lines of credit.

Similarly, a sudden drop in sales due to a recession or a change in consumer preferences could create a liquidity crisis if the business hasn’t planned for such a contingency. Unexpected capital expenditures, such as emergency equipment repairs or regulatory compliance costs, can also quickly deplete a company’s liquidity. Furthermore, changes in interest rates can significantly impact the cost of borrowing and affect the overall financial health of the business, especially for companies with significant debt obligations.

Finally, prolonged legal disputes or unexpected litigation can tie up significant funds, jeopardizing a company’s long-term liquidity. Therefore, comprehensive risk assessment and scenario planning are essential components of effective long-term liquidity management.

Risk Management and Contingency Planning

Effective liquidity management necessitates a proactive approach to risk mitigation. Understanding potential threats to a business’s cash flow and developing robust contingency plans are crucial for ensuring financial stability and preventing crises. Ignoring these aspects can lead to severe consequences, including operational disruptions and even business failure.Proactive risk management involves identifying, assessing, and mitigating potential liquidity risks. This process requires a thorough understanding of a business’s specific circumstances, including its industry, market conditions, and internal operations.

A well-defined plan helps to minimize the impact of unforeseen events and maintain financial resilience.

Potential Liquidity Risks

Businesses face a variety of liquidity risks that can severely impact their ability to meet short-term obligations. These risks can stem from both internal and external factors. Understanding these risks is the first step toward effective mitigation.

- Unexpected decreases in sales revenue: Economic downturns, changes in consumer preferences, or increased competition can lead to a significant drop in sales, reducing cash inflows and potentially creating a liquidity shortfall.

- Increased operating expenses: Rising input costs (raw materials, energy), unexpected repairs, or unforeseen legal issues can strain cash flow and reduce a company’s ability to meet its obligations.

- Delays in payments from customers: Slow-paying clients or a high percentage of outstanding invoices can significantly impact cash flow, particularly for businesses with limited reserves.

- Unexpected debt obligations: Early loan repayments, unexpected interest rate hikes, or unforeseen legal settlements can create sudden liquidity pressures.

- Supply chain disruptions: Events such as natural disasters, pandemics, or geopolitical instability can disrupt supply chains, leading to production delays and increased costs, ultimately affecting cash flow.

Contingency Planning for Liquidity Risks

A well-structured contingency plan Artikels specific actions to be taken in response to various liquidity risk scenarios. This plan should be regularly reviewed and updated to reflect changes in the business environment and the company’s financial position.A comprehensive plan typically includes:

- Early warning system: Establishing key performance indicators (KPIs) and monitoring systems to detect early signs of liquidity stress. This might involve tracking cash flow projections, days sales outstanding (DSO), and debt-to-equity ratios.

- Liquidity buffers: Maintaining sufficient cash reserves or readily accessible lines of credit to cover unexpected expenses or shortfalls in revenue.

- Negotiated credit facilities: Establishing pre-approved credit lines with banks or other financial institutions to provide access to funds during emergencies.

- Cost-cutting measures: Identifying areas where expenses can be reduced in the event of a liquidity crisis, such as reducing non-essential spending or negotiating better terms with suppliers.

- Asset liquidation strategies: Identifying non-essential assets that can be quickly liquidated to raise cash if necessary. This might include selling inventory, equipment, or real estate.

Real-World Examples of Liquidity Crises

Several high-profile businesses have experienced liquidity crises, often due to a combination of factors. These examples underscore the importance of proactive risk management and contingency planning. For instance, the collapse of Lehman Brothers in 2008, triggered by a combination of excessive leverage and a loss of confidence in the financial markets, highlights the devastating consequences of inadequate liquidity management.

Similarly, the struggles faced by numerous retailers during the COVID-19 pandemic, resulting from mandated closures and decreased consumer spending, demonstrated the vulnerability of businesses with insufficient cash reserves and inadequate contingency plans. These cases highlight the critical need for robust liquidity management strategies, including diversification of funding sources, proactive risk assessment, and contingency planning.

Technology and Liquidity Management

Effective liquidity management is significantly enhanced by the strategic implementation of technology. Modern financial software offers businesses powerful tools to monitor cash flow, predict future needs, and automate payments, ultimately leading to improved financial stability and reduced risk. This section explores the crucial role of technology in optimizing liquidity management.

Technology plays a vital role in improving a business’s ability to manage its liquidity. Sophisticated software solutions provide real-time visibility into cash flow, enabling proactive adjustments to financial strategies. This proactive approach, facilitated by technology, allows businesses to avoid potentially damaging cash shortages and optimize their use of available funds. The automation features built into many financial platforms further streamline processes, reducing manual effort and minimizing the risk of human error.

Cash Flow Forecasting and Analysis Tools

Numerous technological tools are available to assist with accurate cash flow forecasting and analysis. These tools often integrate with accounting software, drawing data directly from financial records to produce detailed projections. This eliminates manual data entry, reducing the potential for errors and saving valuable time. Furthermore, advanced analytics features within these tools allow businesses to identify trends, predict potential shortfalls, and optimize their spending and investment strategies.

Examples of such tools include cloud-based accounting software like Xero and QuickBooks Online, which offer integrated forecasting features. More specialized solutions, such as Vena and Anaplan, provide advanced forecasting and planning capabilities, particularly beneficial for larger organizations with complex financial structures. These platforms often incorporate machine learning algorithms to enhance forecasting accuracy by analyzing historical data and identifying patterns that might be missed through manual analysis.

For instance, a business could use these tools to predict seasonal fluctuations in sales and adjust its borrowing needs accordingly.

Benefits of Automated Payment Systems

Automated payment systems offer significant advantages in enhancing liquidity management. By automating invoice processing, payments to suppliers, and payroll, businesses can improve efficiency and reduce the risk of late payments, which can negatively impact credit ratings and relationships with vendors. The precise timing of payments enabled by automation ensures that funds are utilized optimally, avoiding unnecessary delays and optimizing cash flow.

Automated payment systems, such as those offered by platforms like Stripe and PayPal, streamline the payment process, reducing manual intervention and associated errors. This ensures timely payments to suppliers, maintaining positive business relationships and avoiding potential penalties for late payments. Moreover, the improved visibility into payment schedules allows for better cash flow forecasting, enabling businesses to anticipate and manage potential liquidity issues more effectively.

For example, a company can use automated systems to schedule recurring payments to vendors, ensuring that funds are disbursed efficiently and on time, avoiding potential disruptions to their supply chain and improving their creditworthiness.

Illustrating Liquidity Management Challenges

Effective liquidity management is crucial for business survival and growth. A lack of understanding or poor execution can lead to severe financial difficulties, even for otherwise successful companies. This section explores a hypothetical scenario illustrating the challenges businesses face when liquidity management is neglected.A hypothetical scenario involving a rapidly growing e-commerce business, “TrendyThreads,” will be used to illustrate a liquidity crisis.

TrendyThreads experienced a surge in online orders due to a successful marketing campaign. However, their rapid growth outpaced their cash inflows. They invested heavily in inventory to meet the increased demand, but the long payment terms offered to suppliers, coupled with slow customer payments (many using buy-now-pay-later options), created a significant cash flow mismatch. This resulted in a liquidity crisis, where TrendyThreads lacked sufficient cash to meet its immediate obligations, such as paying suppliers, salaries, and rent.

This situation, despite high sales, jeopardized the company’s ability to operate.

TrendyThreads’ Response to the Liquidity Crisis

To overcome the liquidity crisis, TrendyThreads implemented several corrective measures. First, they renegotiated payment terms with their key suppliers, securing shorter payment windows and potentially even partial prepayments. Second, they accelerated their accounts receivable collection process by implementing stricter credit checks for new customers and aggressively pursuing outstanding payments from existing clients. This involved utilizing automated invoicing and payment reminders.

Third, they explored short-term financing options, such as lines of credit and invoice financing, to bridge the cash flow gap. Finally, they revised their inventory management strategy, implementing a just-in-time system to reduce the amount of capital tied up in inventory. These steps helped improve their cash flow and restore their liquidity position.

Visual Representation of Poor Liquidity Management’s Impact

A line graph illustrating the impact of poor liquidity management on profitability could be created. The x-axis would represent time (e.g., months or quarters), and the y-axis would represent both profitability (e.g., net income) and liquidity (e.g., cash on hand). The graph would show a period of strong sales growth initially, reflected in rising profitability. However, concurrently, the line representing cash on hand would begin to decline as the business struggles to manage its cash flow.

As the liquidity situation worsens, the profitability line would eventually start to fall, reflecting the increasing difficulty in meeting operational expenses and investing in growth. The graph would visually demonstrate the interconnectedness of liquidity and profitability, showcasing how poor liquidity management can ultimately undermine even a profitable business. The point where the profitability line starts its decline would clearly highlight the tipping point of the liquidity crisis.

Mastering liquidity management is not a destination but an ongoing journey requiring vigilance and adaptation. By implementing the strategies and insights discussed—from accurate cash flow forecasting and optimized working capital to leveraging technology and proactively managing risks—businesses can significantly enhance their financial stability and unlock greater potential for growth. Remember, proactive planning and a comprehensive understanding of your financial landscape are key to navigating the complexities of liquidity management and ensuring long-term success.

FAQ Resource

What is the difference between liquidity and solvency?

Liquidity refers to a company’s ability to meet its short-term obligations, while solvency refers to its ability to meet its long-term obligations.

How can I improve my company’s Days Sales Outstanding (DSO)?

Improve invoice processing efficiency, offer early payment discounts, and proactively follow up on overdue payments.

What are some early warning signs of a liquidity crisis?

Increasingly late payments from customers, difficulty meeting payroll, supplier payment delays, and consistently negative cash flow.

How can I choose the right short-term financing option for my business?

Consider factors such as interest rates, fees, repayment terms, and the impact on your credit score. Consult with a financial advisor to determine the best fit.