Effective cash flow liquidity management is crucial for business survival and growth. It’s not just about having enough money in the bank; it’s about strategically managing inflows and outflows to ensure operational efficiency and capitalize on opportunities. This involves understanding key metrics, implementing robust forecasting techniques, and leveraging technology to optimize financial processes. Poor cash flow management can lead to missed opportunities, strained supplier relationships, and even bankruptcy, while skillful management fosters resilience and expansion.

This guide delves into the core principles of cash flow liquidity management, exploring strategies for improvement, the role of technology, and the crucial interplay between liquidity and logistics. We’ll examine key metrics, forecasting methods, and risk mitigation techniques, illustrated with real-world examples and case studies to provide a comprehensive understanding of this vital aspect of financial health.

Defining Cash Flow Liquidity Management

Cash flow liquidity management is a critical aspect of financial health for any business, regardless of size or industry. It involves the efficient management of incoming and outgoing cash to ensure the organization can meet its short-term obligations and maintain operational stability. Effective cash flow management is not merely about having enough money; it’s about strategically controlling the timing and amount of cash inflows and outflows to optimize financial performance and minimize risk.Cash flow liquidity management focuses on the short-term financial health of a company, specifically its ability to meet its immediate financial obligations.

It differs from other financial management concepts such as profitability management (which focuses on long-term revenue generation and expense control) and capital budgeting (which focuses on long-term investments). While profitability and capital budgeting are crucial for long-term success, cash flow liquidity management addresses the immediate need for sufficient cash to operate effectively. A profitable company can still fail if it cannot manage its cash flow effectively.

Conversely, a company with strong cash flow liquidity might not be highly profitable but can still survive and thrive in the short term.

Core Principles of Cash Flow Liquidity Management

The core principles revolve around forecasting, controlling, and optimizing cash flows. Accurate forecasting of both inflows and outflows is paramount, allowing for proactive planning and mitigation of potential shortfalls. Controlling cash outflows involves careful budgeting, efficient procurement processes, and timely payment strategies. Optimizing cash inflows requires effective sales management, efficient collection of receivables, and strategic inventory management.

A key aspect is maintaining sufficient cash reserves to act as a buffer against unexpected events or seasonal fluctuations. This proactive approach minimizes the risk of liquidity crises and allows businesses to seize opportunities as they arise.

Defining Cash Flow Liquidity Management: A Detailed Explanation

Cash flow liquidity management is the process of planning, monitoring, and controlling a company’s cash inflows and outflows to ensure it has enough readily available cash to meet its short-term obligations, such as paying suppliers, employees, and debts. This involves forecasting future cash flows, developing strategies to improve cash inflows and manage outflows, and maintaining adequate cash reserves to handle unexpected expenses or fluctuations in business activity.

It’s a proactive approach to managing short-term financial risk, ensuring the company remains solvent and operational. The goal is not just survival but also the ability to take advantage of growth opportunities without facing financial constraints.

Examples of Businesses with Strong and Weak Cash Flow Liquidity Management

The following table illustrates companies with contrasting cash flow liquidity management approaches. The “Cash Flow Liquidity Score” is a hypothetical representation for illustrative purposes and is not based on publicly available data.

| Company Name | Industry | Cash Flow Liquidity Score (1-10) | Key Strategies |

|---|---|---|---|

| Walmart | Retail | 9 | Efficient inventory management, strong supply chain, rapid payment collection, large cash reserves. |

| Apple | Technology | 8 | High-margin products, strong brand loyalty, effective sales forecasting, efficient cost control. |

| (Hypothetical struggling retailer) “RetailCo” | Retail | 3 | Poor inventory management, slow payment collection, high debt levels, insufficient cash reserves. |

| (Hypothetical startup) “InnovateTech” | Technology | 5 | Rapid growth, high burn rate, reliance on external funding, inconsistent cash inflows. |

Key Metrics for Assessing Cash Flow Liquidity

Effective cash flow liquidity management relies on accurate and timely monitoring of key performance indicators (KPIs). These metrics provide a comprehensive view of a company’s ability to meet its short-term obligations and maintain operational stability. Understanding these metrics is crucial for proactive financial planning and risk mitigation.

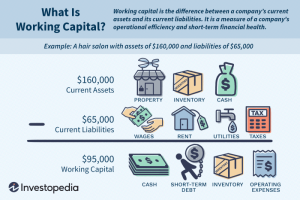

Current Ratio

The current ratio is a fundamental liquidity metric that measures a company’s ability to pay off its current liabilities (due within one year) with its current assets. It provides a snapshot of short-term solvency. The calculation is straightforward:

Current Ratio = Current Assets / Current Liabilities

A higher current ratio generally indicates stronger liquidity. For example, a company with current assets of $500,000 and current liabilities of $250,000 has a current ratio of 2.0, suggesting a healthy liquidity position. Conversely, a ratio below 1.0 signals potential short-term financial distress. However, it’s important to note that an excessively high current ratio might indicate inefficient asset management.

Quick Ratio (Acid-Test Ratio)

The quick ratio, a more conservative measure than the current ratio, excludes inventories from current assets. This is because inventories may not be easily converted to cash. The formula is:

Quick Ratio = (Current Assets – Inventories) / Current Liabilities

Using the previous example, if the company had inventories of $100,000, the quick ratio would be 1.6 ((500,000 – 100,000) / 250,000). A lower quick ratio compared to the current ratio highlights the reliance on inventory conversion to meet short-term obligations.

Cash Ratio

The cash ratio offers the most stringent liquidity assessment, focusing solely on the most liquid assets: cash and cash equivalents. It is calculated as:

Cash Ratio = (Cash + Cash Equivalents) / Current Liabilities

This metric provides a direct measure of a company’s immediate ability to settle its current debts. A high cash ratio indicates a strong ability to meet immediate obligations, while a low ratio signals potential liquidity problems. For instance, if the company in our example had $50,000 in cash and cash equivalents, its cash ratio would be 0.2 ($50,000 / $250,000).

Operating Cash Flow Ratio

The operating cash flow ratio evaluates the ability of a company’s operating activities to cover its current liabilities. It’s calculated as:

Operating Cash Flow Ratio = Operating Cash Flow / Current Liabilities

This ratio provides insights into the sustainability of the company’s liquidity position, focusing on the cash generated from its core operations. A higher ratio indicates a stronger ability to meet short-term obligations through operational cash flow. For example, if the company’s operating cash flow was $300,000, the operating cash flow ratio would be 1.2 ($300,000 / $250,000).

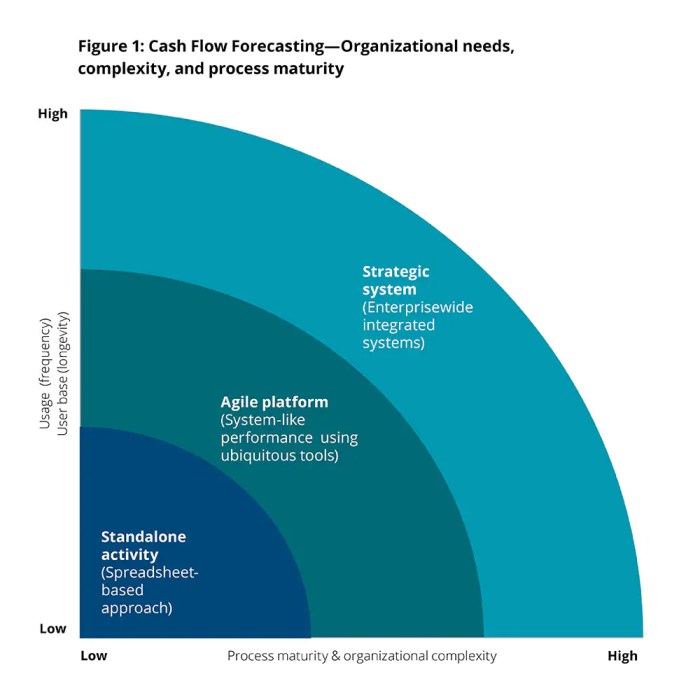

Cash Flow Liquidity Dashboard Design

A dashboard visualizing these key metrics would significantly enhance liquidity monitoring. The dashboard could be designed with a clear and concise layout, using a combination of charts and tables.The dashboard would include:* Data Sources: The data would be sourced from the company’s accounting system, including the balance sheet and cash flow statement. Data would be updated regularly, ideally on a monthly basis.

Visualizations

Key metrics (Current Ratio, Quick Ratio, Cash Ratio, Operating Cash Flow Ratio) would be displayed using bar charts or line graphs over time to show trends. A table summarizing the current values of each metric would also be included.

Color-coding

A color-coding system would highlight any metrics falling outside pre-defined acceptable ranges, immediately drawing attention to potential liquidity issues. For instance, ratios below a certain threshold might be highlighted in red, indicating a need for immediate attention.

Trend Analysis

The graphs would visually display trends over time, allowing for early identification of potential liquidity problems. This would aid in proactive financial planning and decision-making.

Forecasting and Budgeting for Cash Flow Management

Accurate cash flow forecasting and budgeting are crucial for the financial health of any business, regardless of size. These processes provide a roadmap for managing expenses, securing funding, and ultimately achieving financial stability and growth. Without them, businesses risk running out of cash, missing opportunities, and even facing insolvency. A well-structured forecast allows proactive decision-making, enabling businesses to adapt to changing market conditions and capitalize on opportunities.Forecasting and budgeting are intrinsically linked.

Forecasting projects future cash flows based on historical data, market trends, and anticipated sales. Budgeting, on the other hand, translates these forecasts into a plan, allocating resources and setting targets for various aspects of the business. The two processes work in tandem to provide a comprehensive financial picture and guide strategic planning.

Cash Flow Forecasting Methods

Several methods exist for forecasting cash flow, each with its own strengths and weaknesses. The choice of method often depends on factors such as the business’s size, complexity, and data availability.

- Simple Moving Average: This method averages cash flows from previous periods to predict future cash flows. It’s simple to use but may not accurately reflect trends or seasonality.

- Weighted Moving Average: Similar to the simple moving average, but assigns different weights to cash flows from different periods, giving more importance to recent data. This can improve accuracy, especially in dynamic markets.

- Regression Analysis: This statistical method identifies relationships between cash flow and other variables (e.g., sales, production levels) to predict future cash flows. It’s more complex but can provide more accurate forecasts, particularly for businesses with extensive historical data.

- Time Series Analysis: This sophisticated technique analyzes historical cash flow data to identify patterns and trends, using models like ARIMA to predict future cash flows. This approach is suitable for businesses with long historical records and complex patterns.

Sample Cash Flow Budget for a Small Business

The following is a simplified cash flow budget for a hypothetical small bakery called “Sweet Success” for the month of October. This demonstrates how various income and expense categories are incorporated. Note that this is a simplified example and a real-world budget would be far more detailed.

| Item | October |

|---|---|

| Cash Inflows | |

| Sales Revenue | $15,000 |

| Loan Proceeds | $5,000 |

| Total Cash Inflows | $20,000 |

| Cash Outflows | |

| Cost of Goods Sold (Ingredients, etc.) | $6,000 |

| Salaries | $4,000 |

| Rent | $1,500 |

| Utilities | $500 |

| Marketing & Advertising | $1,000 |

| Loan Repayment | $1,000 |

| Total Cash Outflows | $14,000 |

| Net Cash Flow (Inflows – Outflows) | $6,000 |

Risk Management in Cash Flow Liquidity Management

Effective cash flow liquidity management necessitates a proactive approach to risk mitigation. Ignoring potential disruptions can lead to severe financial difficulties, impacting a business’s ability to meet its short-term obligations and hindering its long-term growth. A robust risk management framework is crucial for maintaining financial stability and ensuring the organization’s resilience in the face of unforeseen challenges.

Potential Risks Affecting Cash Flow Liquidity

Several factors can negatively impact a company’s cash flow liquidity. These risks, if not adequately addressed, can create significant financial instability. Understanding these potential threats allows for the development of appropriate mitigation strategies.

- Delayed Customer Payments: Late or non-payment from customers can severely restrict incoming cash flow, particularly for businesses with extended credit terms. This risk is amplified during economic downturns or when dealing with unreliable clients.

- Unforeseen Expenses: Unexpected repairs, equipment failures, or legal issues can drain available cash reserves quickly. Effective budgeting and contingency planning are crucial in mitigating this risk.

- Seasonality in Sales: Businesses with seasonal sales patterns often experience fluctuations in cash flow. Careful planning and proactive measures, such as securing lines of credit, are necessary to bridge periods of low revenue.

- Economic Downturns: Recessions and economic slowdowns can significantly reduce customer demand and increase payment defaults, leading to a sharp decline in cash flow.

- Inventory Management Issues: Holding excessive inventory ties up capital and increases storage costs, while insufficient inventory can lead to lost sales and revenue. Effective inventory management is crucial for optimal cash flow.

Strategies for Mitigating Cash Flow Liquidity Risks

Implementing appropriate mitigation strategies is paramount to safeguarding against the risks Artikeld above. A multi-faceted approach is often most effective.

- Credit Policy Optimization: Implementing stringent credit checks, offering early payment discounts, and factoring invoices can help improve the timeliness of customer payments. Careful consideration of credit limits and payment terms is vital.

- Contingency Planning: Establishing a financial reserve fund for unexpected expenses provides a buffer against unforeseen events. This fund can be supplemented by readily accessible lines of credit or other financing options.

- Cash Flow Forecasting and Budgeting: Accurate forecasting allows businesses to anticipate periods of low cash flow and proactively adjust their spending or secure financing. Regular budgeting ensures financial discipline and helps identify potential cash flow shortfalls.

- Diversification of Revenue Streams: Reducing reliance on a single customer or product can lessen the impact of unexpected revenue drops. Diversification spreads risk and enhances cash flow stability.

- Effective Inventory Management: Implementing a robust inventory management system, utilizing just-in-time inventory strategies, and optimizing stock levels can minimize capital tied up in inventory.

Real-World Application of Risk Management Techniques

Consider a small manufacturing company experiencing consistent delays in customer payments. This directly impacts their ability to pay suppliers and meet payroll obligations.

The key risk here is the reliance on a small number of large clients with extended payment terms. A key mitigation strategy is to diversify their customer base and implement a more stringent credit policy, including credit scoring and shorter payment terms for new clients. This reduces reliance on any single customer and improves the predictability of cash inflows.

This proactive approach, involving both diversification and stricter credit management, significantly reduces the risk of future cash flow shortfalls. The company can also explore factoring their invoices to receive immediate payment for outstanding debts, further strengthening their liquidity position.

Mastering cash flow liquidity management is not merely about reacting to financial pressures; it’s about proactively shaping a business’s financial destiny. By understanding and implementing the strategies discussed – from accurate forecasting and budgeting to leveraging technology and mitigating risks – businesses can build a strong financial foundation, enabling them to navigate economic uncertainties, seize growth opportunities, and achieve long-term sustainability.

Proactive management ensures a company’s ability to meet its obligations, invest in future growth, and ultimately, thrive.

FAQ Overview

What is the difference between cash flow and profitability?

Cash flow refers to the actual movement of money into and out of a business, while profitability reflects the difference between revenues and expenses over a period. A profitable business may still experience cash flow problems if its receivables are slow or it has significant capital expenditures.

How can I improve my accounts receivable turnover?

Implement stricter credit policies, offer early payment discounts, and actively pursue overdue payments. Regularly review customer creditworthiness and consider factoring invoices if necessary.

What are some early warning signs of poor cash flow?

Increasingly late payments to suppliers, difficulty meeting payroll, frequent overdrafts, and a shrinking cash reserve are all warning signs that require immediate attention.

What is the role of a cash flow forecast?

A cash flow forecast projects future cash inflows and outflows, allowing businesses to anticipate potential shortfalls and plan accordingly. This enables proactive management of resources and avoids unexpected financial crises.