Effective liquidity management is crucial for business success. It’s not just about having enough cash on hand; it’s about strategically managing cash flow, mitigating risks, and securing funding to ensure operational stability and growth. This exploration delves into the core principles and practical applications of liquidity management solutions, providing insights for businesses of all sizes.

We will examine various strategies, from accurate cash flow forecasting and working capital optimization to the selection of appropriate funding options and the role of technology in enhancing efficiency. Understanding these aspects is paramount for navigating financial uncertainties and achieving long-term financial health.

Defining Liquidity Management Solutions

Liquidity management solutions are strategies and tools businesses employ to ensure they have enough readily available cash to meet their short-term obligations. Effective liquidity management is crucial for maintaining operational stability, preventing financial distress, and seizing growth opportunities. A well-structured approach allows businesses to balance the need for readily accessible funds with the desire to maximize returns on invested capital.Effective liquidity management solutions incorporate several core components.

These include accurate cash flow forecasting, efficient working capital management, access to diverse funding sources, and robust risk management protocols. A comprehensive system integrates these elements to provide a holistic view of a company’s liquidity position, enabling proactive decision-making.

Core Components of Effective Liquidity Management Solutions

Effective liquidity management relies on a robust framework incorporating several key components. Accurate cash flow forecasting is paramount, providing a clear picture of expected inflows and outflows. This enables businesses to anticipate potential shortfalls and plan accordingly. Efficient working capital management optimizes the use of current assets and liabilities, ensuring a healthy balance between inventory, receivables, and payables.

Diversifying funding sources, such as lines of credit, short-term loans, and commercial paper, provides flexibility and reduces reliance on a single source. Finally, robust risk management, including stress testing and contingency planning, prepares the business for unexpected events that could impact liquidity.

Examples of Liquidity Management Solutions for Various Business Sizes

The optimal liquidity management solution varies significantly depending on the size and complexity of a business. Small businesses might rely on simple cash flow projections and overdraft facilities. Medium-sized enterprises may incorporate more sophisticated forecasting models and explore short-term financing options like factoring or invoice discounting. Large corporations often utilize treasury management systems, sophisticated cash forecasting models, and a diverse portfolio of short-term investments to optimize liquidity.

For instance, a small retail store might use a simple spreadsheet to track cash flow, while a multinational corporation would employ a sophisticated treasury management system integrated with its ERP.

Best Practices for Implementing a Robust Liquidity Management Strategy

Implementing a successful liquidity management strategy requires a structured approach. Regularly reviewing and updating cash flow forecasts is essential to adapt to changing market conditions. Maintaining strong relationships with financial institutions provides access to flexible funding options when needed. Effective working capital management involves optimizing inventory levels, accelerating receivables collection, and negotiating favorable payment terms with suppliers.

Proactive risk management involves identifying potential liquidity risks and developing contingency plans to mitigate their impact. For example, a company might establish a reserve fund to cover unexpected expenses or negotiate a revolving credit facility with its bank.

Key Performance Indicators (KPIs) Used to Measure Liquidity Management Effectiveness

Several key performance indicators (KPIs) are used to assess the effectiveness of a liquidity management strategy. These include the current ratio (current assets / current liabilities), the quick ratio ((current assets – inventory) / current liabilities), and the cash ratio (cash + cash equivalents / current liabilities). These ratios provide insights into a company’s ability to meet its short-term obligations.

Other important metrics include days sales outstanding (DSO), days payable outstanding (DPO), and days inventory outstanding (DIO), which reflect the efficiency of working capital management. Monitoring these KPIs helps businesses identify areas for improvement and ensure their liquidity position remains healthy. For example, a consistently high DSO might indicate inefficiencies in the receivables collection process.

Cash Flow Forecasting and Management

Accurate cash flow forecasting is the cornerstone of effective liquidity management. Understanding your anticipated inflows and outflows allows for proactive planning, mitigating potential shortfalls and maximizing opportunities for growth. Without reliable forecasting, businesses risk insolvency, missed investment opportunities, and difficulty in meeting operational expenses.

Effective cash flow forecasting and management directly impacts a company’s ability to meet its short-term obligations, invest in growth opportunities, and maintain financial stability. A well-managed cash flow streamlines operations, improves creditworthiness, and enhances overall financial health.

Improving Cash Flow Forecasting Accuracy

Improving the accuracy of cash flow forecasts requires a multi-faceted approach. This involves utilizing historical data, incorporating current market trends, and employing robust forecasting techniques.

Several methods contribute to more precise forecasts. Firstly, analyzing historical financial data provides a baseline understanding of past cash flow patterns. Secondly, incorporating external factors such as economic indicators, industry trends, and seasonality allows for a more comprehensive prediction. Finally, leveraging advanced forecasting techniques, like statistical modeling or machine learning algorithms, can significantly improve predictive accuracy.

Optimizing Cash Flow Management

Optimizing cash flow involves implementing strategies to maximize inflows and minimize outflows. This includes efficient invoice processing, optimizing inventory levels, negotiating favorable payment terms with suppliers, and strategically managing accounts receivable.

Techniques for optimizing cash flow include implementing automated invoice processing systems to expedite payments received. Careful inventory management prevents tying up capital in excess stock. Negotiating extended payment terms with suppliers provides more time to generate cash. Finally, robust accounts receivable management, including proactive follow-up on outstanding invoices, ensures timely collection of payments.

Sample Cash Flow Projection

A simple cash flow projection provides a clear overview of expected cash inflows and outflows over a given period. Below is a sample projection table:

| Month | Inflows | Outflows | Net Cash Flow |

|---|---|---|---|

| January | $50,000 | $40,000 | $10,000 |

| February | $60,000 | $45,000 | $15,000 |

| March | $70,000 | $55,000 | $15,000 |

| April | $55,000 | $48,000 | $7,000 |

This table illustrates a simplified projection. A real-world projection would incorporate far more detail, including specific sources of inflows (sales, investments, etc.) and categories of outflows (salaries, rent, materials, etc.). The level of detail required will depend on the size and complexity of the business.

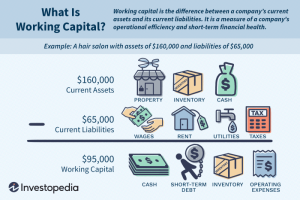

Working Capital Management

Effective working capital management is crucial for maintaining a healthy liquidity position. It involves strategically managing current assets and liabilities to ensure the smooth operation of a business and its ability to meet short-term financial obligations. A well-managed working capital cycle directly contributes to improved liquidity, enabling businesses to seize opportunities and weather financial challenges.Working capital is the difference between a company’s current assets (like cash, accounts receivable, and inventory) and its current liabilities (like accounts payable, short-term debt, and accrued expenses).

Liquidity, on the other hand, refers to a company’s ability to meet its short-term obligations as they come due. The relationship is direct: sufficient working capital provides the resources necessary to meet those obligations, thereby enhancing liquidity. Conversely, insufficient working capital can strain liquidity, leading to potential financial difficulties.

Optimizing Working Capital for Improved Liquidity

Strategies for optimizing working capital focus on efficiently managing current assets and liabilities. This involves accelerating cash inflows and slowing down cash outflows. Effective strategies include optimizing inventory levels to minimize storage costs and obsolescence while ensuring sufficient stock to meet demand, negotiating favorable payment terms with suppliers to extend payment periods, and implementing efficient collection procedures to shorten the days sales outstanding (DSO).

Furthermore, exploring financing options like short-term loans or lines of credit can provide a buffer during periods of cash flow constraint. A well-structured approach to working capital management can significantly improve a company’s ability to meet its immediate financial obligations.

Inventory Management’s Impact on Liquidity

Inventory represents a significant portion of a company’s current assets. Inefficient inventory management can tie up significant capital, reducing liquidity. Holding excessive inventory leads to increased storage costs, potential obsolescence, and a higher risk of losses. Conversely, insufficient inventory can lead to lost sales and dissatisfied customers. Effective inventory management requires accurate forecasting of demand, efficient ordering processes, and robust inventory tracking systems.

Techniques like Just-In-Time (JIT) inventory management can help minimize inventory levels while ensuring sufficient stock to meet demand, thus optimizing liquidity. For example, a car manufacturer implementing JIT would receive parts only when needed for immediate assembly, reducing storage costs and improving cash flow.

Best Practices for Managing Accounts Receivable and Payable

Efficient management of accounts receivable and payable is paramount for maintaining healthy liquidity. Effective management of accounts receivable involves implementing robust credit policies, monitoring outstanding invoices closely, and employing efficient collection procedures. This includes setting clear payment terms, promptly following up on overdue payments, and considering factoring or invoice discounting to accelerate cash inflows. For example, a company offering a 2% discount for early payment might encourage quicker settlements and reduce days sales outstanding (DSO).Optimizing accounts payable involves negotiating favorable payment terms with suppliers, taking advantage of early payment discounts where beneficial, and maintaining good relationships with vendors.

This allows for better cash flow management and improves the company’s negotiating power. For instance, negotiating extended payment terms with suppliers provides more time to generate cash before payments are due.

Funding and Financing Options

Effective liquidity management necessitates a thorough understanding of available funding and financing options. Choosing the right source depends heavily on a company’s specific financial situation, risk tolerance, and long-term goals. This section will explore various short-term and long-term financing strategies, highlighting their advantages and disadvantages to aid in informed decision-making.Short-term and long-term financing options differ significantly in their terms, costs, and suitability for various liquidity needs.

Short-term options provide immediate relief but often come with higher interest rates, while long-term options offer lower costs but require a longer commitment. The selection process involves careful consideration of factors like the amount of funding required, the duration needed, and the potential impact on the company’s credit rating.

Comparison of Short-Term and Long-Term Financing Options

Short-term financing, typically used for bridging temporary cash flow gaps, includes options like lines of credit, commercial paper, and short-term loans. Long-term financing, on the other hand, addresses more substantial capital needs and longer-term projects, encompassing options such as term loans, bonds, and equity financing. The choice between them hinges on the nature and duration of the liquidity challenge.

For instance, a seasonal shortfall might necessitate a short-term line of credit, while significant expansion plans could justify a long-term loan or bond issuance.

Advantages and Disadvantages of Specific Funding Sources

Lines of credit offer flexibility, allowing businesses to borrow funds as needed up to a pre-approved limit. However, interest rates can be variable and subject to market fluctuations. Commercial paper, on the other hand, is a short-term unsecured promissory note issued by large corporations, offering a relatively low-cost funding source but limited to creditworthy entities. A company might opt for a line of credit for its unpredictable operational expenses, whereas a financially robust company with a strong credit rating might prefer commercial paper for its lower interest costs.

Factors to Consider When Selecting a Funding Option

Several key factors influence the selection of an appropriate funding option. These include the cost of capital (interest rates, fees), the repayment terms, the impact on the company’s financial ratios (e.g., debt-to-equity ratio), the availability of collateral, and the flexibility offered by the financing instrument. A company with limited collateral might find it challenging to secure a loan, potentially leading them to explore other options like equity financing.

Conversely, a company with strong assets could leverage them to secure favorable loan terms.

Decision Tree for Choosing an Appropriate Funding Source

The following decision tree provides a simplified framework for selecting a funding source. It should be noted that this is a simplified representation and a more detailed analysis is typically required.

| Question | Answer | Funding Option |

|---|---|---|

| Is the funding needed for short-term or long-term needs? | Short-term | Line of Credit, Commercial Paper |

| Long-term | Term Loan, Bonds, Equity Financing | |

| What is the company’s credit rating? | Strong | Commercial Paper, Term Loan (favorable terms) |

| Weak | Line of Credit (potentially higher interest), Equity Financing | |

| Is collateral available? | Yes | Term Loan (potentially lower interest) |

| No | Line of Credit, Equity Financing |

Technology and Liquidity Management

Technology plays a crucial role in modern liquidity management, transforming it from a manual, time-consuming process into a dynamic, data-driven function. Effective technology integration allows businesses to gain real-time visibility into their cash flows, predict potential shortfalls, and optimize their funding strategies. This leads to improved efficiency, reduced risk, and enhanced profitability.The implementation of technology significantly enhances the accuracy and speed of liquidity management processes.

Manual processes are prone to errors and delays, whereas automated systems can process vast amounts of data quickly and accurately, providing a more comprehensive and reliable picture of the company’s financial health. This improved accuracy allows for better forecasting and more informed decision-making.

Software Solutions for Liquidity Management

Numerous software solutions are available to support liquidity management, ranging from simple spreadsheet-based tools to sophisticated enterprise resource planning (ERP) systems with integrated treasury modules. These tools automate various tasks, including cash forecasting, bank reconciliation, and reporting. The choice of software depends on the size and complexity of the organization, its specific needs, and its budget.

Best Practices for Technology Implementation

Successful technology implementation requires careful planning and execution. This includes defining clear objectives, selecting appropriate software, integrating the system with existing systems, providing adequate training to users, and establishing robust data governance procedures. A phased approach, starting with a pilot project before full-scale deployment, can minimize disruption and maximize the chances of success. Regular system reviews and updates are also essential to maintain efficiency and accuracy.

Data Analytics and Liquidity Management Decision-Making

Data analytics plays a vital role in enhancing decision-making in liquidity management. By analyzing historical data, market trends, and other relevant information, businesses can gain valuable insights into their cash flow patterns, identify potential risks, and optimize their liquidity strategies. For example, predictive analytics can forecast future cash flows with greater accuracy, enabling businesses to proactively manage potential shortfalls.

This proactive approach minimizes the risk of liquidity crises and allows for better resource allocation. Furthermore, the use of dashboards and reporting tools allows for quick visualization of key metrics, enabling faster and more informed decision-making.

Liquidity Management and Logistics Management

Liquidity management and logistics management, while seemingly disparate, share significant interconnectedness. Both are crucial for the efficient and profitable operation of any business, impacting each other in subtle yet powerful ways. Understanding their interplay is vital for optimizing overall business performance.

Key Principles and Practices: A Comparison

Liquidity management focuses on ensuring a company has sufficient readily available funds to meet its short-term obligations. This involves careful cash flow forecasting, efficient working capital management, and strategic funding options. In contrast, logistics management centers on the efficient flow and storage of goods, from procurement to delivery to the end consumer. This includes inventory management, transportation, warehousing, and supply chain optimization.

While liquidity management deals primarily with financial flows, logistics management deals with the physical flow of goods. However, both aim to minimize costs and maximize efficiency.

Points of Intersection and Interdependence

The intersection of these two fields lies primarily in their impact on working capital. Efficient logistics directly impacts inventory levels and the speed of receivables collection. Reduced inventory holding times, facilitated by optimized logistics, free up capital that can be used to improve liquidity. Conversely, delays and inefficiencies in the supply chain can tie up capital, straining liquidity.

For instance, delays in receiving raw materials can disrupt production, leading to missed sales and increased borrowing needs. Similarly, slow collection of receivables, potentially due to logistical issues in delivery, reduces available cash.

Effective Logistics Management’s Contribution to Improved Liquidity

Effective logistics contributes to improved liquidity in several ways. Just-in-time (JIT) inventory management, a core principle of efficient logistics, minimizes warehousing costs and reduces the capital tied up in inventory. Streamlined transportation and distribution networks ensure timely delivery of goods, leading to faster payment from customers and improved cash flow. Optimized warehousing reduces storage costs and minimizes the risk of obsolescence or damage to inventory, preserving capital.

Furthermore, efficient logistics can lead to reduced costs across the entire supply chain, freeing up resources that can be allocated to bolster liquidity.

Inefficiencies in Logistics and Their Negative Impact on Liquidity

Inefficiencies in logistics can significantly hinder liquidity. Delays in shipping and receiving can lead to production stoppages, missed sales opportunities, and increased storage costs. Damage to goods during transit requires costly replacements, impacting profitability and available cash. Poor inventory management can result in stockouts, lost sales, and ultimately, reduced cash inflows. Overstocking, on the other hand, ties up significant capital in unsold inventory, diminishing liquidity.

For example, a company experiencing port congestion due to poor logistical planning might face delays in receiving crucial raw materials, leading to production halts and a subsequent decrease in cash flow. This scenario highlights the direct link between logistical inefficiencies and reduced liquidity.

Mastering liquidity management is a continuous process of assessment, adaptation, and optimization. By implementing robust strategies, leveraging technological advancements, and maintaining a proactive approach to risk mitigation, businesses can build a strong financial foundation and navigate the complexities of the modern economic landscape with confidence. The key lies in a holistic approach that integrates financial planning, operational efficiency, and informed decision-making.

FAQ Guide

What is the difference between liquidity and solvency?

Liquidity refers to a company’s ability to meet its short-term obligations, while solvency refers to its ability to meet its long-term obligations.

How often should a business review its liquidity position?

Regular review, ideally monthly or quarterly, is recommended to identify potential issues early and make timely adjustments.

What are some early warning signs of liquidity problems?

Decreasing cash balances, difficulty meeting payments, increasing reliance on short-term debt, and declining sales are potential indicators.

Can a business be profitable yet still experience liquidity problems?

Yes, profitable businesses can face liquidity issues if their cash flow is poorly managed or if they have significant receivables or inventory.